Comprehensive vs. Collision Auto Insurance Coverage in 2025 (Differences Explained)

Comprehensive vs. collision auto insurance coverage differ in cost and protection. Comprehensive coverage starts at $25/mo and protects your vehicle against theft, weather damage, vandalism, and other non-collision incidents. Collision coverage starts at $61/mo and covers damages resulting from accidents.

Free Car Insurance Comparison

Compare Quotes From Top Companies and Save

![]() Secured with SHA-256 Encryption

Secured with SHA-256 Encryption

Kalyn Johnson

Insurance Claims Support & Sr. Adjuster

Kalyn grew up in an insurance family with a grandfather, aunt, and uncle leading successful careers as insurance agents. She soon found she has similar interests and followed in their footsteps. After spending about ten years working in the insurance industry as both an appraiser dispatcher and a senior property claims adjuster, she decided to combine her years of insurance experience with another...

Insurance Claims Support & Sr. Adjuster

UPDATED: Nov 19, 2024

It’s all about you. We want to help you make the right coverage choices.

Advertiser Disclosure: We strive to help you make confident auto insurance decisions. Comparison shopping should be easy. We are not affiliated with any one auto insurance provider and cannot guarantee quotes from any single provider.

Our insurance industry partnerships don’t influence our content. Our opinions are our own. To compare quotes from many different companies please enter your ZIP code on this page to use the free quote tool. The more quotes you compare, the more chances to save.

Editorial Guidelines: We are a free online resource for anyone interested in learning more about auto insurance. Our goal is to be an objective, third-party resource for everything auto insurance related. We update our site regularly, and all content is reviewed by auto insurance experts.

UPDATED: Nov 19, 2024

It’s all about you. We want to help you make the right coverage choices.

Advertiser Disclosure: We strive to help you make confident auto insurance decisions. Comparison shopping should be easy. We are not affiliated with any one auto insurance provider and cannot guarantee quotes from any single provider.

Our insurance industry partnerships don’t influence our content. Our opinions are our own. To compare quotes from many different companies please enter your ZIP code on this page to use the free quote tool. The more quotes you compare, the more chances to save.

On This Page

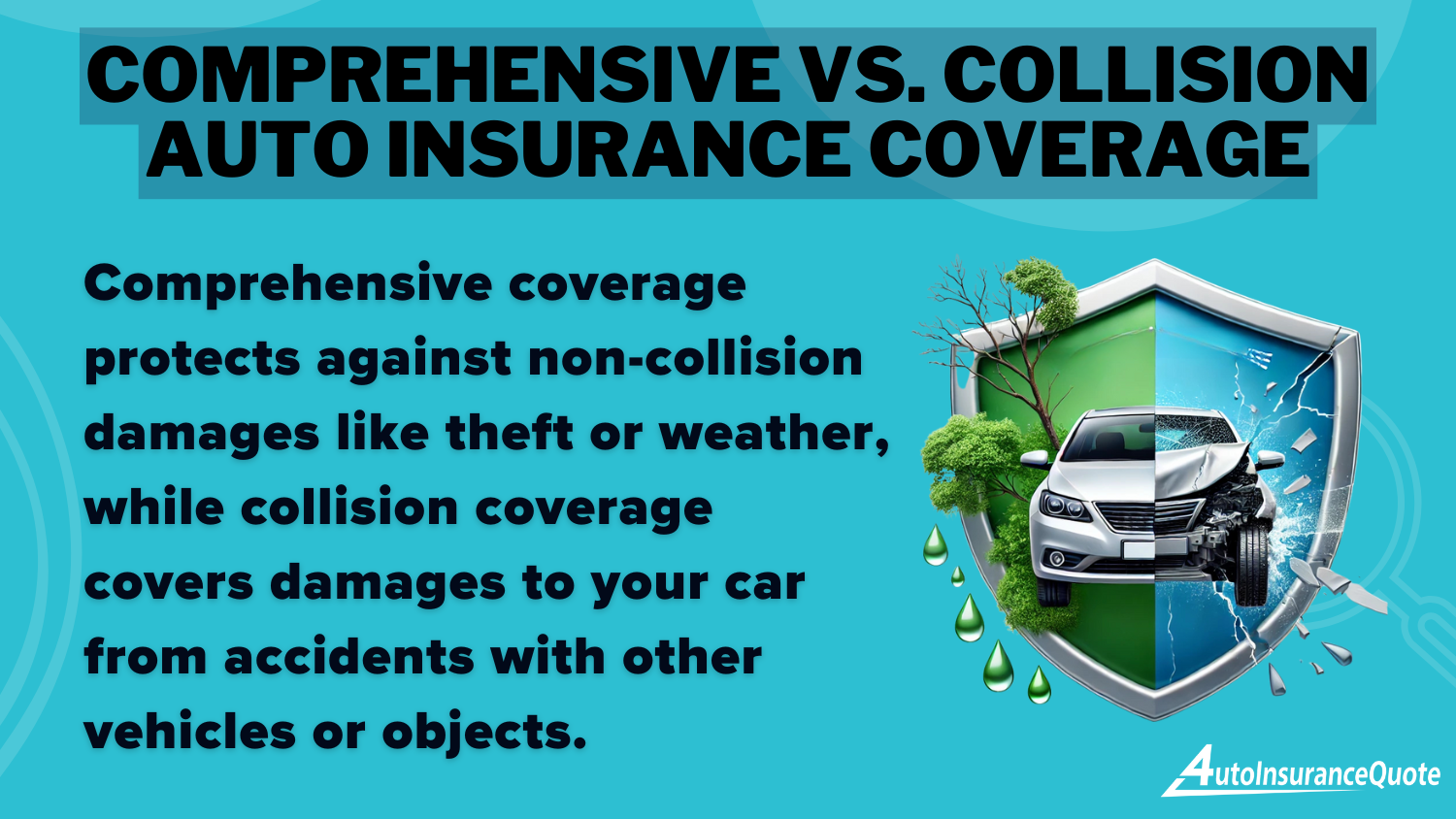

Comprehensive vs. collision auto insurance coverage are two key options that you should consider for vehicle protection. Comprehensive coverage protects against non-collision incidents like theft, vandalism, and weather-related damage, while collision coverage pays for repairs after an accident, regardless of fault.

The choice between the two types of insurance coverage depends on factors such as your vehicle’s value and in accordance with your budget constraints.

For you to get the best rates, you must compare quotes from leading providers such as Progressive, Geico, and State Farm to ensure you’re getting the right protection for the best price.

Read More: Does auto insurance cover damage done by a shopping cart?

Get fast and cheap auto insurance coverage today with our quote comparison tool above.

- Collision covers accident damage to your vehicle, regardless of fault

- Comprehensive covers theft, vandalism, and weather damage

- The best choice depends on your vehicle’s value, risk tolerance, and budget

Collision Coverage Explained

Collision coverage is an optional car insurance policy that helps pay for repairs or replacement of your vehicle if it’s damaged in an accident, regardless of fault. Unlike basic liability insurance, which only covers damage to other vehicles or property, collision coverage protects your own car.

If your vehicle is damaged in an accident, your insurance will cover the repair costs minus your deductible. If the repair costs exceed the vehicle’s value, your insurer will declare it “totaled” and provide compensation based on the car’s value.

Comprehensive vs. Collision Auto Insurance Coverage Monthly Rates by Provider| Insurance Company | Comprehensive Coverage | Collision Coverage |

|---|---|---|

| $35 | $75 | |

| $30 | $65 | |

| $25 | $60 | |

| $40 | $80 | |

| $30 | $65 | |

| $41 | $85 | |

| $34 | $70 | |

| $32 | $68 | |

| $28 | $61 | |

| $45 | $90 |

Collision coverage also applies in cases where you were not at fault, with your insurer covering the repair costs and seeking reimbursement from the other driver’s insurance.

It is especially useful in hit-and-run accidents where the at-fault driver is unknown, as it covers damage to your car even if the responsible driver cannot be identified. This coverage ensures you are financially protected regardless of who caused the accident.

Read More: Does my auto insurance cover damage to my own car if I am at fault in an accident?

Compare over 200 auto insurance companies at once!

![]() Secured with SHA-256 Encryption

Secured with SHA-256 Encryption

Comprehensive Coverage Explained

Comprehensive coverage is an optional insurance policy that covers your vehicle in a broader range of situations – including storm damage, theft, and vandalism.

When you just buy collision coverage, your vehicle is only covered in an accident. With comprehensive coverage, you get extended coverage for situations outside of accidents.

Differences Between Collision and Comprehensive Auto Insurance| Type of coverage | Purpose | What's covered | What's not covered |

|---|---|---|---|

| Comprehensive | Covers repair/replacement costs if the car is damaged by anything other than a collision with another vehicle or someone's property | Vandalism, theft, fire, hail, falling objects, animals, water damage, and much more | Crashes into objects and accidents involving two or more vehicles (regardless of fault); see "Full Coverage" |

| Collision | Covers repair/replacement costs if the car is damaged as the result of a collision with another vehicle or someone else's property | Crashes into objects and accidents involving two or more vehicles (regardless of fault) | Vandalism, theft, fire, hail, falling objects, animals, water damage, and much more; see "Full Coverage" |

| Full Coverage | While not really a type of coverage itself, this term is often used to describe comprehensive and collision coverage when bundled together | Everything shown in "Comprehensive" and "Collision" | Damage to other vehicles, medical expenses, lost wages as the result of an accident, and numerous other expenses which drivers need other types of insurance to cover |

Comprehensive coverage provides protection against a variety of risks not typically covered by basic car insurance. Some of the major things covered by comprehensive insurance include vandalism, theft, flood damage, and damage from fallen objects like tree branches.

It also covers damage caused by hail, fires, and other non-collision events, offering broad protection for your vehicle against unexpected circumstances.

In many cases, comprehensive coverage also covers other vehicles you drive – like rental cars or a friend’s car. Explore how affordable comprehensive auto insurance coverage protects your vehicle from unexpected risks while fitting your budget.

Buying Both Comprehensive and Collision Coverage

Basic liability insurance is required by law, but collision and comprehensive coverage are optional. While these coverages come at a higher cost, they provide extensive protection for your vehicle. A comparison of comprehensive auto insurance shows how both cover vandalism, theft, and accidents, offering full coverage vs collision coverage for more peace of mind in almost any situation.

It’s important to understand the difference between collision and comprehensive coverage—comprehensive covers non-collision incidents like theft, hail, or vandalism, while collision covers accident repairs.

Also, consider the comprehensive deductible vs. collision deductible when choosing your policy. Comprehensive vs collision coverage with Progressive provides flexibility and options depending on your needs and vehicle value.

Ultimately, your decision will depend on your comfort with risk and the value of your vehicle. If you’re willing to pay more today for more protection, both coverages may be worth it. If not, removing one or both could save you money, though it leaves you with higher financial risk in certain situations.

Read more: Does auto insurance cover vandalism?

You May Be Required to Carry Collision or Comprehensive Coverage

In some cases, you may be required to carry both collision and comprehensive coverage for the insured vehicle. For example, if you finance or lease your vehicle, the lender or dealership will usually require you to have these coverages.

This is to protect their investment in your vehicle, as it serves as collateral for the loan. Understanding the difference between collision and comprehensive auto insurance can help clarify your coverage options.

From hail to vandalism, comprehensive insurance coverage may help pay for repairs. Know what to consider when deciding your deductible. Learn more: https://t.co/fYVJX8sEEO pic.twitter.com/eYVyljWVLF

— USAA (@USAA) November 28, 2022

While comprehensive vs. collision loss covers non-collision damages like theft or weather, collision coverage vs. comprehensive coverage specifically handles accident-related repairs.

Once your vehicle is paid off, you can choose to remove these coverages, as the lender no longer has a claim on your vehicle. Learn more about the different types of auto insurance coverage to find the right protection for your vehicle and make informed decisions about your policy.

Compare over 200 auto insurance companies at once!

![]() Secured with SHA-256 Encryption

Secured with SHA-256 Encryption

When to Drop Collision and Comprehensive Coverage

You buy car insurance to protect your vehicle, which is why most people choose comprehensive vs collision auto insurance. Generally, it’s a good idea to include both as long as you can afford the premiums. However, there are situations where you may want to drop collision and comprehensive coverage to lower your costs.

A common rule of thumb is the 10% rule. This suggests dropping comprehensive vs collision auto insurance if the cost of the premiums exceeds 10% of your car’s book value.

For instance, if your car is worth $3,000, and your premiums cost $320 per year, it may be worth dropping this extra coverage. You could also look for cheap comprehensive and collision insurance if you still want to maintain coverage while saving money.

If you’re comfortable with assuming more risk and need to cut costs, dropping optional coverage might be a good option for you. Discover how affordable collision auto insurance coverage can protect your vehicle and help you save money with options that fit your budget and needs.

Comprehensive vs. Collision Auto Insurance: Making the Right Choice

Collision coverage pays for damage to your vehicle if it is involved in an accident, regardless of who is at fault. Comprehensive coverage protects your vehicle from non-accident-related incidents such as theft, flooding, vandalism, and damage caused by falling branches.

When we are to compare comprehensive coverage vs. full coverage, it is best and essential for us to understand that full coverage generally includes both comprehensive and collision coverage.

Additionally, comprehensive and collision coverage are often optional, this will allow the drivers to select the policies that best suit their needs.

Comprehensive insurance covers non-accident risks like theft and weather, while collision insurance covers accident-related damage.Maria Hanson Insurance and Finance Writer

Drivers with a hit-and-run accident may benefit from comprehensive or collision coverage, which provides protection when the responsible party cannot be identified.

While having both types of coverage offers extensive protection, some drivers of older vehicles may consider removing collision coverage to lower their premiums, particularly if the cost of coverage exceeds the car’s value.

To achieve optimal protection, as a policyholder adding both comprehensive and collision coverage is ideal. However, for older vehicles, dropping these optional coverages might be a practical choice based on the vehicle’s value and the driver’s budget.

Read more: Understanding How Auto Insurance Works

Start comparing total coverage auto insurance rates by entering your ZIP code below.

Frequently Asked Questions

What is the difference between comprehensive and collision coverage?

Collision coverage covers the cost of repairing or replacing your vehicle if it’s damaged in an accident, while comprehensive coverage covers a broader range of situations, including storm damage, theft, and vandalism.

Should I buy both comprehensive and collision coverage?

Adding both comprehensive and collision coverage to your policy provides more extensive coverage, but it also increases the cost. It’s ultimately up to you to decide based on your needs and budget. If you’re just looking for coverage to drive legally, enter your ZIP code below to compare cheap auto insurance quotes near you.

When should you drop collision and comprehensive coverage?

Dropping collision and comprehensive coverage may be considered when the cost of premiums exceeds 10% of the book value of your vehicle. It can also be an option if you’re comfortable assuming more risk and need to save money on your premium.

Read more: Does my auto insurance cover damage caused by a blown tire?

Are collision and comprehensive coverage required?

Collision and comprehensive coverage are optional, but if you finance or lease your vehicle, the lender may require you to have them to protect their collateral. Once your vehicle is paid off, you can choose whether to keep or remove the coverage.

What situations are covered by comprehensive insurance?

Comprehensive coverage protects your vehicle in various non-accident-related situations such as storm damage, theft, vandalism, falling objects, fire, and more. It may also cover other vehicles you drive, like rental cars.

Is collision coverage the same as full coverage?

No, collision coverage is not the same as full coverage. Full coverage generally includes comprehensive, collision, and liability coverage. Collision coverage specifically covers damage to your vehicle from accidents, while full coverage provides additional protection against non-accident-related incidents through comprehensive coverage. Learn more about what an auto insurance policy looks like to explore coverage options and choose the best protection for your vehicle and budget.

Is collision insurance more expensive than other types?

Yes, collision insurance is often more expensive than other types of auto insurance, such as comprehensive or liability coverage. This is because collision insurance directly protects your vehicle, regardless of fault, which increases its cost. Factors like your car’s value, driving history, and where you live—such as cities like Chicago or Miami—can also influence the price.

Is it worth having both comprehensive and collision coverage?

Yes, it is worth having both comprehensive and collision coverage for newer or high-value vehicles. This combination offers extensive protection against accidents, theft, vandalism, and natural disasters. However, for older cars with low market value, the cost of premiums might not be justified, making it less practical to maintain both coverages.

Does comprehensive or collision cover hit-and-run accidents?

Yes, comprehensive hit-and-run coverage or collision coverage can provide protection in such situations. Collision coverage typically pays for damages caused by a hit-and-run accident, while comprehensive coverage addresses other risks like vandalism or theft. Together, they offer peace of mind in cases where the at-fault driver cannot be identified.

Read more: Does my auto insurance cover damage caused by a falling object?

When should you consider removing full coverage from your auto insurance?

It would be best if you considered removing full coverage when the cost of maintaining comprehensive and collision coverage exceeds the value of your car. This is usually the case for older vehicles with lower resale value. By evaluating your vehicle’s worth and your financial situation, you can decide if removing full coverage is a cost-effective choice.

Compare over 200 auto insurance companies at once!

![]() Secured with SHA-256 Encryption

Secured with SHA-256 Encryption

Kalyn Johnson

Insurance Claims Support & Sr. Adjuster

Kalyn grew up in an insurance family with a grandfather, aunt, and uncle leading successful careers as insurance agents. She soon found she has similar interests and followed in their footsteps. After spending about ten years working in the insurance industry as both an appraiser dispatcher and a senior property claims adjuster, she decided to combine her years of insurance experience with another...

Insurance Claims Support & Sr. Adjuster

Editorial Guidelines: We are a free online resource for anyone interested in learning more about auto insurance. Our goal is to be an objective, third-party resource for everything auto insurance related. We update our site regularly, and all content is reviewed by auto insurance experts.