Pleasure Use vs Commuter Auto Insurance in 2025 (Differences Explained)

Pleasure use vs commuter auto insurance rates differ. Pleasure use auto insurance averages $83 per month, while commuter use coverage is $95 per month. An auto insurance comparison for pleasure and commute usage shows how driving habits affect premiums, helping you select the most affordable coverage.

Free Car Insurance Comparison

Compare Quotes From Top Companies and Save

![]() Secured with SHA-256 Encryption

Secured with SHA-256 Encryption

Brad Larson

Licensed Insurance Agent

Brad Larson has been in the insurance industry for over 16 years. He specializes in helping clients navigate the claims process, with a particular emphasis on coverage analysis. He received his bachelor’s degree from the University of Utah in Political Science. He also holds an Associate in Claims (AIC) and Associate in General Insurance (AINS) designations, as well as a Utah Property and Casual...

Licensed Insurance Agent

UPDATED: Nov 14, 2024

It’s all about you. We want to help you make the right coverage choices.

Advertiser Disclosure: We strive to help you make confident auto insurance decisions. Comparison shopping should be easy. We are not affiliated with any one auto insurance provider and cannot guarantee quotes from any single provider.

Our insurance industry partnerships don’t influence our content. Our opinions are our own. To compare quotes from many different companies please enter your ZIP code on this page to use the free quote tool. The more quotes you compare, the more chances to save.

Editorial Guidelines: We are a free online resource for anyone interested in learning more about auto insurance. Our goal is to be an objective, third-party resource for everything auto insurance related. We update our site regularly, and all content is reviewed by auto insurance experts.

UPDATED: Nov 14, 2024

It’s all about you. We want to help you make the right coverage choices.

Advertiser Disclosure: We strive to help you make confident auto insurance decisions. Comparison shopping should be easy. We are not affiliated with any one auto insurance provider and cannot guarantee quotes from any single provider.

Our insurance industry partnerships don’t influence our content. Our opinions are our own. To compare quotes from many different companies please enter your ZIP code on this page to use the free quote tool. The more quotes you compare, the more chances to save.

On This Page

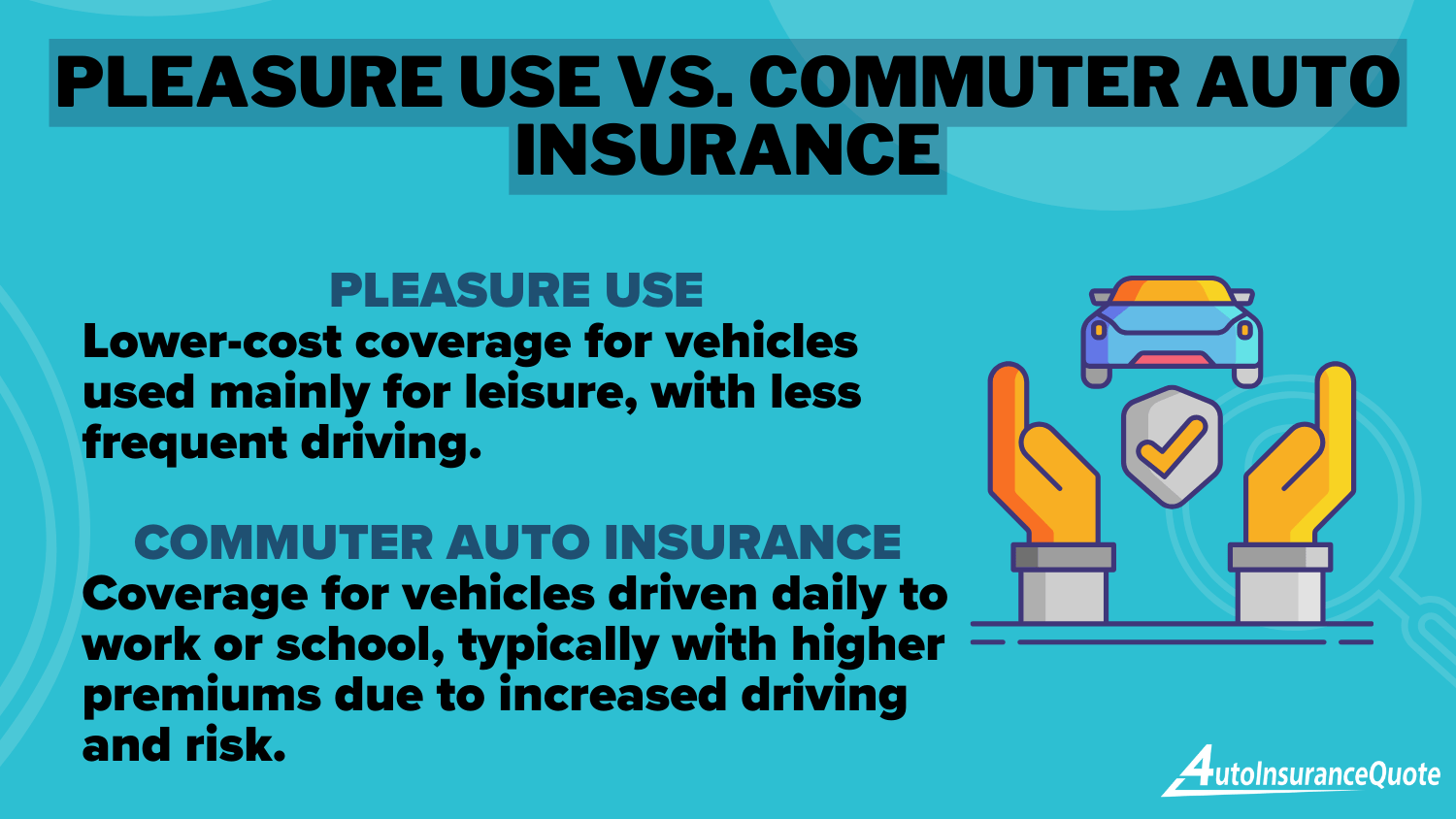

Pleasure use vs commuter auto insurance is key to choosing the best plan for your needs. Pleasure use insurance typically covers vehicles driven infrequently, like for weekend trips or errands, and averages $83 per month in premiums.

In contrast, commuter insurance, designed for cars used daily for work or school, averages $95 per month due to increased risk from frequent driving. When comparing the two, consider how often and how far you drive, along with the impact of peak-hour traffic.

Commuters who travel long distances during rush hours usually pay higher premiums. This guide helps you understand how your driving habits affect your premiums and assists you in finding the most affordable coverage.

Read more: Affordable Roadside Assistance Coverage

Find the best auto insurance company near you by entering your ZIP code into our free quote tool above.

- Pleasure use insurance is cheaper with less frequent driving

- Commuter insurance costs more due to higher mileage and traffic

- Compare both to find the best coverage for your needs

The Difference Between Pleasure Use vs Commuter Auto Insurance

The difference between pleasure and commuter auto insurance comes down to how often you use your car. A “commuter” vehicle is used daily for work, while a “pleasure” vehicle is for non-commuting activities like errands or weekend trips.

When choosing auto insurance for commuting or pleasure, keep in mind that commuting habits vary. Some people drive long distances, while others only travel short distances.

Pleasure Use vs. Commuter Auto Insurance Monthly Rates by Provider| Insurance Provider | Pleasure Use Rate | Commuter Use Rate |

|---|---|---|

| $92 | $110 | |

| $88 | $102 | |

| $91 | $109 | |

| $85 | $95 | |

| $95 | $115 | |

| $87 | $98 | |

| $88 | $100 | |

| $90 | $105 | |

| $89 | $104 | |

| $83 | $97 |

Auto insurance comparison for pleasure use and commute can help you understand the coverage differences. Auto insurance is typically cheaper for pleasure use than for commuting, making it important to know how your car is used to select the right coverage.

Explore our guide on whether a long commute affects your auto insurance rates to understand how your driving habits might impact your premiums and to help you make the best choice for your budget.

Commuter Auto Insurance: Explained

Commuter auto insurance is often chosen by drivers who use their vehicles primarily for work travel, making it type of insurance that is most commonly used for those with daily commutes. This type of insurance is designed to cover the risks associated with regular work-related trips.

When applying, you’ll typically need to specify if your car is for personal or considered a commuter auto insurance policy, which provides protection for frequent, routine work travel.

An example of commuter includes driving from home to an office, college campus, or job site. This is useful for understanding what qualifies for commuter insurance coverage, as different driving patterns bring unique risks.

For drivers using their vehicles mainly for commuting, the best category of auto insurance considers factors like daily mileage and peak travel times. Choosing a policy that fits commuter needs can ensure suitable coverage and possibly lower premiums.

Read more: How Biking Instead of Driving Can Help You Save on Auto Insurance

Pleasure Use Auto Insurance: Explained

Pleasure use auto insurance applies to cars used for non-work activities, like errands or weekend trips. Auto insurance rates are often lower for pleasure use compared to work use, as these cars are driven less and present a lower risk. This makes pleasure use insurance a more affordable option for those not using their car for daily commuting.

On the other hand, commuting is cheaper than pleasure in some cases, as commuters may qualify for discounts, but car insurance for pleasure is cheaper than for commuting overall. Commuters usually drive more during peak hours, which increases the likelihood of accidents. Therefore, insurance premiums are typically higher for commuter vehicles.

Read more: Do you need special insurance coverage to use your car for work?

Compare over 200 auto insurance companies at once!

![]() Secured with SHA-256 Encryption

Secured with SHA-256 Encryption

Why Insurance Companies Ask About Your Commuting Habits

Insurance companies ask if you use your car for “commuting” or “pleasure” to better understand the definition of domestic and pleasure use. This helps them assess the risk involved and adjust your premiums accordingly.

For example, types of auto insurance you do not need can be excluded if commuting is not a regular part of your driving. Cars used for commuting generally drive more miles, which increases the chances of an accident, explaining the disadvantages of commuter auto insurance.

Commuter auto insurance typically costs more than pleasure use insurance due to the increased risk from daily driving and peak-hour traffic.Tonya Sisler Insurance Content Team Lead

The number of miles driven annually plays a major role. A car used for commuting might cover 10,000 miles a year, whereas a pleasure car may only travel 5,000 miles. What commuting includes, such as frequent long trips or highway driving, impacts accident risk and, in turn, the rate an insurance company charges for coverage.

Explore the best low-mileage auto insurance discounts to discover how driving fewer miles could save you money and help you find the ideal coverage for your needs.

Pleasure Use vs Commuter: How to Proceed With Your Car Insurance

Many insurance companies provide simple options to help you choose the right coverage. Instead of just asking whether your car is for “commuting” or “pleasure,” they may inquire if it’s your primary or secondary vehicle. This makes the process easier, as the primary vehicle is generally the one you drive most often.

In addition to primary or secondary usage, some companies will allow you to specify whether the car is a commuter vehicle and estimate its annual mileage. By gathering all of this information, you can get a more accurate quote that reflects how you actually use your car.

The top 5 commercials have been chosen and the Best of GEICO is almost over. But don’t worry: you could still save money with GEICO. 1. Go here: https://t.co/4vjt0fUfxn 2. Make sure you get a fast, free car insurance quote. #bestofgeico pic.twitter.com/j51fAoejwb

— GEICO (@GEICO) February 6, 2019

If you’re still unsure, reviewing the fine print can help. Insurance providers often clarify the types of driving that count as “commuting” or define what qualifies as a primary vehicle. If you’re uncertain, calling the insurance provider directly for clarification can help ensure you choose the right coverage, whether online or by phone.

Read more: What is the difference between primary and secondary auto insurance coverage?

Get fast and cheap auto insurance coverage today with our quote comparison tool below.

Frequently Asked Questions

What is the difference between pleasure use and commute auto insurance?

Commute and pleasure use auto insurance refer to two different types of coverage based on the purpose of your vehicle usage. Commute use insurance typically covers vehicles that are primarily used for commuting to and from work or school. Pleasure use insurance, on the other hand, covers vehicles that are used for non-work-related purposes, such as leisure activities or personal errands.

Why is it important to distinguish between commute and pleasure use for auto insurance?

Distinguishing between commute and pleasure use is important for auto insurance because the purpose for which you use your vehicle can impact your risk profile and, consequently, your insurance rates. Commute use typically involves more time on the road during peak traffic hours, which increases the likelihood of accidents. Insurers consider this higher risk when determining premiums. Pleasure use, on the other hand, is generally associated with lower risk, as it involves less frequent and less congested driving conditions. If you’re just looking for coverage to drive legally, enter your ZIP code below to compare cheap auto insurance quotes near you.

How does auto insurance define “commute” and “pleasure use”?

The specific definitions of “commute” and “pleasure use” may vary between insurance companies, so it’s essential to check with your insurer for their specific guidelines. In general, “commute” typically refers to driving your vehicle to and from a regular place of work or school, while “pleasure use” encompasses personal driving for non-work-related activities, such as grocery shopping, visiting friends, or going on vacations.

Read more: What are the different types of auto insurance coverage?

Can I use my vehicle for both commuting and pleasure while still having coverage?

Yes, it is possible to have coverage for both commute and pleasure use. Many insurance policies provide coverage for both types of usage. However, it’s crucial to disclose accurately how your vehicle will be used by your insurance provider. Failing to provide accurate information about your usage may result in coverage gaps or potential claim denials.

Will my premiums be higher if I use my vehicle for commute purposes?

Generally, yes. Commute use is associated with a higher risk of accidents due to increased traffic and congestion during peak hours. As a result, insurers often charge higher premiums for vehicles primarily used for commuting. However, insurance rates are influenced by various factors, including your driving history, location, vehicle type, and other personal details. It’s best to consult with your insurance provider to understand how your commute usage might affect your premiums.

What if I change my vehicle’s usage from commute to pleasure or vice versa?

If you change your vehicle’s usage from commute to pleasure or vice versa, it’s crucial to inform your insurance provider promptly. Failure to update your policy with accurate usage details may result in coverage issues. Your insurer may need to adjust your policy or provide you with a different type of coverage based on your new vehicle usage. It’s always recommended to notify your insurance company of any changes to ensure you have appropriate coverage in place.

Read more: Affordable Full Coverage Auto Insurance

What qualifies as a commuter vehicle?

A commuter vehicle is a car that is primarily used for traveling to and from work or school on a regular basis. It is typically driven daily and often during peak hours, focusing on long-distance travel between home and the workplace.

Who is defined as a commuter?

A commuter is someone who regularly travels from their home to a fixed destination, like work or school, using a car or public transportation. The key factor is the routine nature of the travel for work or educational purposes, often happening on weekdays.

Is commuting the same as traveling?

No, commuting and traveling are not the same. Commuting specifically refers to the regular journey between home and work or school. Traveling, on the other hand, can include any trip, such as for leisure or business, and doesn’t have to be routine or daily. Discover the average cost of auto insurance to learn about pricing trends and get tips on securing a policy that fits your budget.

Which type of motor vehicle is typically used for social, domestic, and leisure purposes?

Motor vehicles used for social, domestic, and leisure purposes are usually “pleasure use” vehicles. These are cars that are primarily used for activities like running errands, visiting friends or family, or going on vacations rather than commuting to work or school.

What rights does a commuter have?

Commuters have the right to travel safely on public roads without discrimination. They can also access public transportation and parking, and if they are involved in an accident while commuting, they can file for insurance claims depending on their policy. Additionally, commuters are protected under labor laws regarding travel to and from their workplace.

Which insurance coverage is best for a car: pleasure use or commuter?

The best coverage depends on how you use your car. If your car is mainly used for daily travel to work, commuter coverage is ideal as it is designed for regular, work-related trips. However, if your car is used for personal activities like errands or vacations, pleasure use coverage, which is usually cheaper, would be a better choice. Check out affordable auto insurance companies with great customer service to compare options and find the perfect balance of price and service for your needs.

Compare over 200 auto insurance companies at once!

![]() Secured with SHA-256 Encryption

Secured with SHA-256 Encryption

Brad Larson

Licensed Insurance Agent

Brad Larson has been in the insurance industry for over 16 years. He specializes in helping clients navigate the claims process, with a particular emphasis on coverage analysis. He received his bachelor’s degree from the University of Utah in Political Science. He also holds an Associate in Claims (AIC) and Associate in General Insurance (AINS) designations, as well as a Utah Property and Casual...

Licensed Insurance Agent

Editorial Guidelines: We are a free online resource for anyone interested in learning more about auto insurance. Our goal is to be an objective, third-party resource for everything auto insurance related. We update our site regularly, and all content is reviewed by auto insurance experts.